Date the Rate, Marry the House

So all of this “Date the Rate, Marry the House” talk is a great sales pitch but did you know the average marriage lasts 7-8 years and the average homeowner will keep their home for ~13 years. The reality is, sh*t happens and not everyone’s life is perfect. Look at Kim Kardashian’s marriage with Kris Humphries for example… it lasted a WHOPPING 72 days 😂. Relationships and Homeownership both have their ups and downs and there’s more reasons to buy and sell real estate than most people think. Just like there will be plenty of different reasons for someone to refinance (it’s not always about the rate).

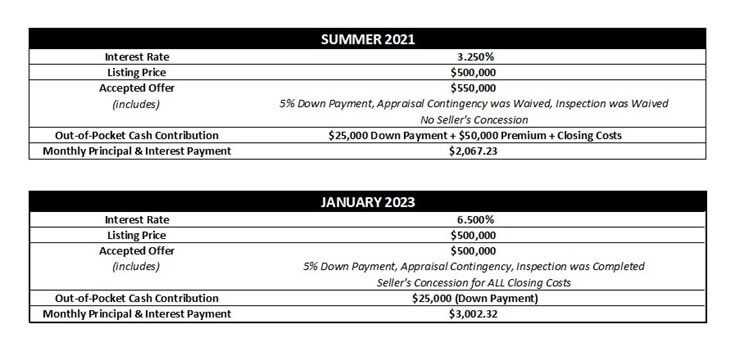

With that said, I think a lot of people are missing the big picture. Let's look at the numbers...

There are two main takeaways from the above examples:

- Purchasing a property today with the same parameters Summer of 2021 requires a significantly smaller out-of-pocket contribution. The buyers from the Summer of 2021 not only had to cover their own closing costs but they also had to pay a $50,000 premium to have their offer accepted.

- Although interest rates are nearly double where they were in the Summer of 2021, the reality is, interest rates will not be back in the 2% - 3% range again anytime soon. If you are waiting for rates to come down – a 5.000% rate by the end of 2023 is wishful thinking for most – and even at 5.000% your monthly principal & interest payment would still be $2,549.90.

While the summer of 2021 involved over-paying, buyer contingencies and in many cases submitting 100 offers to get one accepted, the market we’re currently in involves under paying, seller financing and submitting ONE offer to get one accepted. If you were okay with waiting in hour long lines at open houses to fall in love with a house just to find out a cash buyer overpaid $100,000 for it, then you should be ecstatic about receiving a private showing, seller financing to cover ALL of your closing costs and keeping all of the normal contingencies to protect you as a buyer.

Being a buyer or seller in any market will always have its pros and cons. The shift we’ve seen recently from a seller’s market to a buyer’s market is providing buyers with the following advantages:

- NONE or less buyer contingencies

- Seller’s concessions to help with paying closing costs or obtaining a temporary buydown

- LESS competition

For anyone planning on waiting for one of the following: (1) interest rates to come down or (2) home prices to come down… I PROMISE you aren’t the only one “waiting” and guess what happens when that time comes… MORE competition (bidding wars, contingencies and you can most certainly say goodbye to seller financing such as seller’s concessions).

With that being said, this market serves as a unique opportunity for buyers. Especially those that have sufficient income and credit but don’t necessarily have the funds saved up to buy on their own. Rather than spending another 6-12 months living in your parent’s basement saving up that extra $20,000 for closing costs; negotiate a seller’s concession in your offer. The trade-off… an extra $100-$150/month towards your monthly mortgage payment. Sound doable? THEN STOP SAVING AND START SHOPPING!

One other thing that people fail to realize is that by renting you’re paying 100% interest into your landlord’s pocket. Guess what happens when these landlords start buying properties with higher interest rates? They’re going to need to cover those higher monthly payments to cash flow on the property, which in turn, means higher monthly rent amounts across the board! Now if your rent is going up, but your income is staying the same, how are you expecting to save more money?

We may be in “sales” but this business isn’t just about selling people. It’s about providing consumers with insightful and educational information to help them make one of the biggest financial decisions of their life. STOP selling people on a bullsh*t narrative you heard in your recent sales meeting or on a social media post. “Date the Rate, Marry the House” may sound nice, but what happens if rates don’t fall back below 5% for the next 7-8 years? That’s a long, dragged-out, engagement if you ask me…

Let’s stop making assumptions about the future – nobody has a crystal ball – and make decisions based on the present. Oh and if you’re going to pitch something, pitch the BENEFITS!

Feel free to contact me directly with any questions or concerns pertaining to the numbers and/or financing.

Disclaimer: All information provided in this publication is for informational and educational purposes only, and in no way is any of the content contained herein to be construed as financial, investment, or legal advice or instruction. CrossCountry Mortgage, LLC (“CrossCountry”) does not guarantee the quality, accuracy, completeness or timelines of the information in this publication. While efforts are made to verify the information provided, the information should not be assumed to be error free. Some information in the publication may have been provided by third parties and has not necessarily been verified by CrossCountry.