How Credit Works – and How to Boost Your Score

Throughout your life, you’ve probably received plenty of advice on how to navigate the waters of “adulting.” As you grew up, you took on new responsibilities, starting small and simple with tasks like doing the dishes or the laundry. As you get older, you take on larger responsibilities, such as getting your first job or purchasing your first car. But there is one very important thing that not enough people take into consideration as they come into adulthood – CREDIT!

Everyone knows your credit score has a significant impact on your quality of life, so why isn’t there more emphasis placed on learning about it? The Koutsos Team wants you to know your credit score is more than just a number, so we are going to take a few minutes today to break down exactly how your score is calculated and steps you can take to build and repair your credit in preparation for purchasing a home.

How credit works.

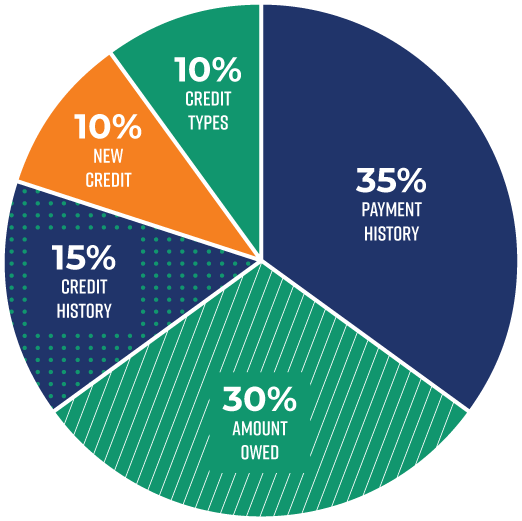

Let’s discuss how credit works. Here’s a visual representation breaking down exactly what plays into calculating your score and how each category is weighted:

Credit Types – 10%.

This is also referred to as your “credit mix.” It is important to note that credit mix is not a one-size-fits-all; what works for you may not work for someone else. It is a good idea to have a variety of different credit to show you can responsibly manage different kinds of debt.

Now you may be wondering, “What do you mean by a variety of credit?” This brings us to our next topic: installment credit versus revolving credit. Don’t let these fancy words scare you. You’ll find simple explanations for both kinds of credit below!

Installment credit includes loans like mortgages, auto loans, student loans, or private/personal loans. These loans are paid on a fixed schedule, with interest, for the term of the loan.

As an example, let’s talk about an auto loan. You know how much you will be paying, on what day, and for how long. This is the perfect example of installment credit.

On the other hand, a good example of revolving credit is credit cards. Because you are not borrowing a lump sum of money, there is no set payment plan. Your minimum payments are based on how much you have borrowed. You can borrow up to a certain amount if you do not exceed your limit. While revolving credit is a little more flexible, it often can result in a lower borrowing amount with higher interest rates.

In more cases than not, revolving credit is a riskier way to borrow than installment credit. The thing to keep in mind is carrying high balances can drag your credit score down. Many people take out installment loans to pay off revolving credit. There are advantages and disadvantages to this method, but we’ll take a deeper dive into that in another blog.

New Credit – 10%.

This category is also referred to as “inquiries.” To put this in simple terms, 10% of your credit score is based on how often/how many times your credit has been recently pulled. Your credit is pulled every time you apply for a new line of credit, like an auto loan or a credit card. There are two different types of inquiries: soft inquiries and hard inquiries.

Soft inquiries do not impact your score. Good examples of soft inquiries are receiving credit card pre-approvals in the mail, job related inquiries, account reviews, and personal credit pulls.

Hard inquiries appear when you apply for some form of credit, like car loans, student loans, mortgages and new credit cards. These inquiries stay on your credit report for two years. It’s important to note tha, if you’re shopping around, multiple reports for mortgage or auto loans within a period of 45 days only counts as 1 inquiry. Additionally, only the first ten inquiries count per year, and each inquiry knocks your score down an average of 5 points.

Credit history – 15%.

Credit history is simple. The longer your credit history, the higher your score. Long credit history and good payment history will have a positive impact on your credit. An extremely important tip: don’t close credit accounts! Say you have a credit card you rarely use. Rather than close the account, use it once a month for some smaller expenses, such as gas, and pay it off. Why? Closing accounts increases your balance to limit ratio and will have a negative impact on your credit score.

One way to help your credit history is to be added as an authorized user to the account of an individual who has a high credit score. This poses no risk to the account holder because they are the one who holds the credit card. You will not actually use the card – you will just be riding the coattails of their good credit and longer credit history!

Amount owed – 30%.

This can also be referred to as balanced carried. Above we quickly mentioned balance to limit ratio, so let’s explain how it works. You are going to want to keep your balance to limit ratio below 30%. Basically, this means you do not want to owe more than 30% of the amount of credit you are eligible to utilize.

Let’s say you have three credit cards:

- Visa with a balance of $4,000, available credit $10,000.

- Mastercard with a balance of $5,000, available credit $10,000.

- Discover with a balance of $0, available credit $10,000.

This brings your total balances to $9,000 and total available credit to $30,000. Now, how do you calculate your balance to limit ratio?

- $9,000/$30,000 = 0.30 x 100 = 30%

To take it a step further, let’s break down the balance to limit ratio on each individual card in order to show you how to maximize your credit score:

- Visa: $4,000/$10,000 = 0.40 x 100 = 40%

- Mastercard: $5,000/$10,000 = 0.50 x 100 = 50%

- Discover: $0/$10,000 = 0%

To maximize your score, it would be wise to move some of the amount owed over to the Discover card. If you were to take $1,000 from the Visa and $2,000 from the Mastercard and move it to Discover, all the cards would be at a 30% balance to limit ratio!

Payment history – 35%.

Now for the big kahuna, the category that has the largest impact on your credit score – payment history! The reason this weighs so heavily on your credit is because is determines if you are deemed a “risk” to a lender. To put it bluntly, do not be late on your payments!

Things that can impact your score include late or missing payments, accounts reported to collections, liens, foreclosures, bankruptcy, and judgements.

Keep in mind even one late payment can be detrimental to your score. You can work with your creditors to remove late payments from your credit score, but it will just take a bit of elbow grease. Call your creditor and request they remove the late payment(s). Once they agree, ask for an official letter from them stating the date, the individual you worked with to remove the late payment, and that the late payment will be removed. It is imperative to document these interactions to ensure your creditors follow through with removing any late payment.

Steps to improve your score.

What can you do to improve your score before purchasing a home?

- Pay your bills on time and pay past due accounts.

- Work with your creditors to remove erroneous late payments.

- Have credit limits increased to improve your balance to limit ratio.

- Become an authorized user on someone else’s account.

- Do not close old accounts or dispute anything on your credit report.

If you have any questions regarding credit and credit scores, please reach out to us. The Koutsos Team has a passion for helping first-time homebuyers realize their dream of homeownership, and we would love to help start you on your journey!