Understanding 1031 Exchange Purchases

A 1031 exchange is a powerful tax-deferral strategy that allows real estate investors to sell an investment or business property and reinvest the proceeds into another “like-kind” property without immediately paying capital gains taxes. Named after Section 1031 of the Internal Revenue Code, this strategy is commonly used to preserve equity, grow portfolios, and reposition investments. However, successfully completing a 1031 exchange requires strict adherence to specific rules—especially the time requirements.

What Is a 1031 Exchange Purchase?

In a 1031 exchange, the purchase of the replacement property is the final and most critical step. After selling the relinquished property, the investor must reinvest the proceeds into one or more qualifying replacement properties. These properties must be held for investment or business use and must be of like-kind, which broadly includes most real estate used for investment purposes.

The purchase itself must be structured correctly, with exchange funds held by a qualified intermediary (QI) and never directly received by the investor. Failure to follow these requirements can disqualify the exchange and trigger immediate tax liability.

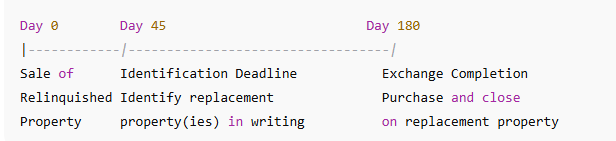

Key Time Requirements at a Glance

A 1031 exchange operates on two overlapping timelines that begin the day the relinquished property closes.

These are calendar days, not business days, and extensions are generally not allowed.

The 45-Day Identification Period

The first and most time-sensitive requirement in a 1031 exchange is the 45-day identification period. This period begins on the day the relinquished property closes.

Within 45 calendar days, the investor must formally identify potential replacement properties in writing to the qualified intermediary. The identification must be unambiguous and follow one of the IRS-approved identification rules, such as:

- Three-Property Rule: Identify up to three properties, regardless of value

- 200% Rule: Identify more than three properties as long as their total value does not exceed 200% of the relinquished property’s value

No extensions are allowed, even if the 45th day falls on a weekend or holiday. Missing this deadline will invalidate the exchange.

The 180-Day Exchange Period

The second major deadline is the 180-day exchange period. The investor must close on one or more of the identified replacement properties within 180 calendar days of the sale of the relinquished property—or by the due date of the investor’s tax return for that year, whichever comes first.

This means the purchase of the replacement property must be completed within this timeframe, using the exchange funds held by the qualified intermediary. Just like the identification period, the 180-day deadline is absolute and cannot be extended except in rare circumstances such as federally declared disasters.

Planning for a Successful Purchase

Because the timelines are strict, advance planning is critical. Many investors begin searching for replacement properties before selling their current property. Others consider alternatives such as reverse exchanges or improvement exchanges when timing or inventory constraints exist.

Working with experienced professionals—real estate agents, qualified intermediaries, tax advisors, and lenders—can help ensure the purchase is completed correctly and on time.

Why Timing Matters

The time requirements are one of the most common reasons 1031 exchanges fail. Delays in negotiations, financing issues, or unexpected closing problems can easily push a transaction beyond the allowed periods. Understanding these deadlines and preparing early can make the difference between a successful exchange and an unexpected tax bill.

Conclusion

A 1031 exchange purchase offers investors a valuable opportunity to defer capital gains taxes and reinvest in stronger or more suitable properties. However, the benefits come with strict rules—especially the 45-day identification period and the 180-day exchange period. By understanding these time requirements and planning accordingly, investors can execute a compliant exchange and continue building long-term wealth through real estate.