First‑time buyers really are getting older, homeowners really do have far more wealth than renters, and when I layer in what has actually happened to prices and equity in Charlotte since 2015, the “cost of waiting” becomes impossible to ignore. In this version, I want to show the chart, then walk through a very real‑world example of a buyer who purchased in 2015 and what that decision has meant for their net worth by 2025.

How old first‑time buyers are now

When I sit with first‑time buyers, I start by grounding them in the big picture. National data show the median age of first‑time buyers around 38 today, up from about 33 just a few years ago and the late 20s in the early 1990s. Many media pieces now round that to “about 40” for the average first‑time buyer, which is very different from the traditional image of a late‑20s couple buying their starter home.

So more people are waiting an extra decade to buy that first house. That delay shortens the amount of time they have for equity to build, mortgages to amortize, and appreciation to compound before they hit key milestones like kids in college or retirement.

Why owners are so much wealthier than renters

I then connect that age shift to net worth. Looking at Federal Reserve data, recent analyses put the median homeowner’s net worth in the low‑to‑mid $400,000 range, versus around $10,400 for the median renter. That’s roughly a 40–43x gap in wealth, and for many families, home equity is the single biggest reason for the difference.

When I explain this, I say it plainly: most owners have hundreds of thousands in net worth; most renters have just a few thousand. That gap didn’t appear overnight; it’s the result of years of mortgage payments quietly reducing principal while home values rise over time.

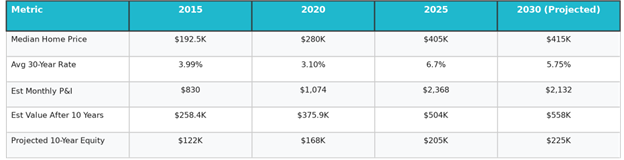

The Charlotte chart: price, payment, and 10‑year equity

Because I’m in the Charlotte area, I like to translate those national themes into local numbers. Here’s a simplified snapshot using median prices, typical mortgage rates, and estimated 10‑year value and equity for someone buying in different years with 10% down on a 30‑year fixed.

Charlotte, NC – Median Home, 10% Down, 30‑Year Fixed

Projected equity = 10% down + 10 years of principal reduction + 10 years of assumed 3% annual appreciation, all rounded for illustration.

I use this table as an educational tool, not a promise. It shows how even with conservative assumptions, a decade of ownership can translate into six‑figure equity, especially when you start earlier.

The real 2015 Charlotte buyer: what actually happened

But in Charlotte, those conservative 3% annual gains turned out to be far too low. Prices here have grown much faster, with multiple reports showing that home values in many parts of the region have essentially doubled over a relatively short window.

So I walk clients through a “real” example like this, in first person:

- Let’s say I bought the median Charlotte home in 2015 for about $192,500.

- I put 10% down, which is about $19,250 of immediate equity.

- Fast‑forward to 2025, and median prices are in the $400,000‑plus range—roughly $405,000 in many 2025 reports for a typical Charlotte resale home.

Now, instead of a conservative 3% annual gain, that move from $192,500 to about $405,000 over 10 years is more like a compound annual appreciation rate of roughly 7–8%, depending on the exact data set. That is a huge tailwind for wealth building.

On top of the appreciation, I’ve also been paying down my mortgage for a decade. If I started with a standard 30‑year fixed around 4% in 2015 (close to the national average that year), by 2025 I’ve knocked down a meaningful chunk of principal. A reasonable, rounded estimate looks like this:

- Home value in 2025: ≈ $405,000

- Remaining loan balance after 10 years: roughly $130,000–$140,000 on that original loan amount

- Estimated equity today: about $260,000–$270,000

So instead of the ≈$122,000 “textbook” 10‑year equity from the conservative chart, a real 2015 Charlotte buyer could easily be sitting on around a quarter of a million dollars in equity by 2025.

When I share that story, I’m not trying to cherry‑pick the hottest possible outcome. I’m simply using the actual path Charlotte has taken:

- Starting price: very attainable sub‑200s in 2015.

- Strong, above‑average local appreciation for a decade.

- Ten years of steady amortization on a relatively low‑rate 30‑year fixed.

That is exactly how ordinary middle‑income households in this market end up on the “homeowners have 40x the net worth of renters” side of the ledger.

What this means for someone thinking about buying now

Once I’ve walked through that 2015 example, I bring it back to the person sitting across from me. I say something like this in first person:

- If you had bought that median Charlotte home in your 30s in 2015, you might be looking at $250,000‑plus in equity today. That’s not a theoretical number; it’s what the market has actually delivered to many owners over the last decade.

- If you’re only starting your buying journey in 2025, your starting price is higher, your rate is higher, and you have 10 fewer years for appreciation and amortization to work before 2035 than that 2015 buyer did before 2025.

- If you wait again—say until 2030—you compress that timeline even further and risk missing another whole equity cycle, just as renters did from 2015 to 2025.

I’m very clear that no one can guarantee another 10‑year run like Charlotte just had, and I don’t pretend that prices only move in one direction. But the pattern is consistent:

- The people who own during long stretches of time capture the upside of appreciation and pay down debt every month.

- The people who rent through those stretches pick up the entire housing bill without building the asset.

So when someone asks whether waiting 5 or 10 years to buy their first home really matters, this is how I answer in the first person:

Yes, it matters—a lot. If owning a home is part of your long‑term plan, and you wait through periods like 2015–2025 in Charlotte, you’re not just postponing a decision; you may be passing up the chance at hundreds of thousands of dollars of equity that could support retirement, college for kids, or a move‑up home later on. My job is to help you buy responsibly, but also to make sure you understand that time in the market is just as powerful for homeowners as it is for investors.

About the Author

This article was written by Chester J Wisinski with CrossCountry Mortgage. Chet is a mortgage loan officer serving the Charlotte, NC market, specializing in first‑time homebuyers and educational programs for real estate professionals.

Data Sources and Acknowledgments

Market data and statistics referenced in this article are drawn from publicly available reports and datasets, including:

- National Association of REALTORS® home buyer and housing market reports

- Federal Reserve household net worth surveys

- Local MLS and Realtor association reports for the Charlotte, NC region

- UNC Charlotte “State of Housing in Charlotte” and related research

- Major mortgage rate and housing data aggregators (e.g., Freddie Mac, FRED, and national rate surveys)

Copyright Notice

© 2025 Chester J Wisinski. All rights reserved. This article may not be reproduced, distributed, or transmitted in any form without prior written permission of the author, except for brief quotations used in reviews, social media posts, or educational settings with attribution.

Published December 2025

For more information or to discuss your homebuying options in Charlotte, NC, please contact a qualified mortgage lender in your area.

The information provided is for educational purposes only and should not be considered financial, investment, or legal advice. All numbers, examples, and scenarios are illustrative only and not guaranteed; results may vary based on borrower qualifications, loan program requirements, and market conditions. The views and opinions expressed are those of the author and do not necessarily reflect the views of CrossCountry Mortgage, LLC (“CrossCountry”).